While the material has actually been Have a peek at this website thoroughly examined, we can not as well as do not guarantee that the details offered is proper, exact or current. Please talk with your Rothenberg Wealth Administration consultant for guidance based on your unique conditions. Rothenberg Funding Administration is a member of IIROC and the Canadian Financier Security Fund. If a reverse mortgage has substantially reduced the equity of your residence, there might be little financing delegated cover long-lasting treatment later in life. You generally have up to a year after leaving to either market or generate the repayment, Pfau states. The classification of non-borrowing spouse, created in 2015, implies the continuing to be partner can continue to be in the house.

The percentage of house equity you maintain will lower in time, and also can also decrease to no. If you're age 60, one of the most you can obtain is likely to be 15-- 20% of the worth of your residence. So, at 65, one of the most you can borrow will be about 20-- 25%.

Chris- I would say you have actually not efficiently offered your home with a reverse home loan. You can market the home, re-finance the home, you can transform instructions anytime. There are no manacles with the HECM, it merely provides you much more choices and adaptability if the scenarios of your retirement need them. For anyone still lugging a balance, that most likely implies replacing an inexpensive home mortgage with something much more expensive. The reason for higher prices as well as costs on 2nd as well as third home loan has historically been the higher threat from the key lien owner confiscating after default. It does not make any type of feeling for the HECM lender to get all the extra advantages that include extra threat when there is efficiently no danger at all to making the funding.

- As the article notes, the little girl of one reverse-mortgage borrower sent in a form showing she intended to acquire the property and also was accepted for conventional funding.

- When you think of borrowing against the equity you have in your house, proceed with care before you turn what is most likely your greatest asset right into an atm machine.

- The truth is reverse home loans are exorbitantly pricey finances.

- I would go as far as how much is time share to say that if you select to do this, pay back nearly the whole amount owed however leave a very small equilibrium of just a couple hundred dollars on the car loan unpaid.

If you've dealt with obstacles creating the cash for these important costs, adding to your debt should not get on the table. As opposed to making a settlement every month, you will certainly pay nothing. The passion cost is included in the mortgage equilibrium, so in the second month, the balance expands. Considering that the car loan equilibrium is currently a little larger, the passion expense is a touch greater, and this procedure continues up until the moment comes for the financing to be repaid. That payment typically happens within one year of when you move out of https://messiahxcnm667.bcz.com/2022/01/30/current-home-mortgage-rates/ the home or when you die. When a reverse home loan is registered against the title of your residence, you might be unable to utilize your residence to secure any kind of future borrowing.

Reverse Home Loans Might Be Helpful In Retirement If You Mind The Risks

You stay in your residence as well as do not need to make payments while living there. Passion charged on the car loan compounds in time, so it gets bigger as well as contributes to the amount you borrow. The interest rate is most likely to be more than on a typical mortgage. If among the property owners dies, the partner or the other individual on title can continue to reside in the residence without needing to resolve the financing. Nevertheless, once both homeowners have died, the administrator needs to supply HomeEquity Financial institution with a death certificate immediately.

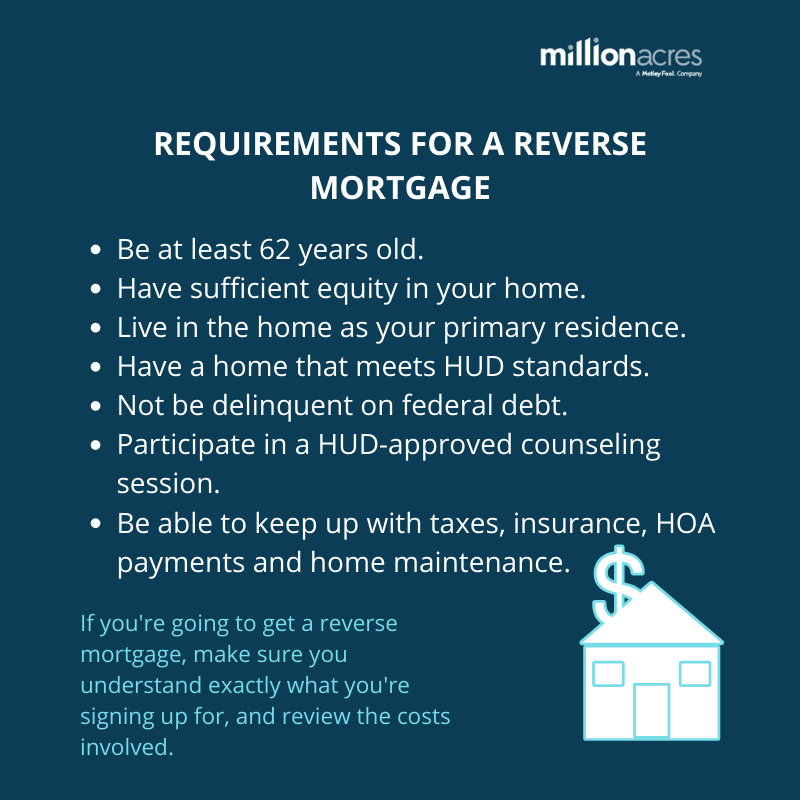

On your reverse mortgage application, you should include all the people listed on your residence's title. All these individuals have to go to the very least 55 years of ages to be eligible. Nevertheless, this can be done using other funds or by re-financing with a traditional home loan. The funding is safeguarded versus real estate you, or your partner, very own in Australia. You pay a charge for the deal as well as to obtain your house valued (as an overview, around $2,000).

The vast majority of reverse mortgages are guaranteed via the Federal Real Estate Administration,, which suggests if the financial debt is not paid back by the borrower, it will certainly be repaid with FHA reserves. A reverse home mortgage can be established to make regular repayments to a property owner, or it can be taken as a round figure. In either instance, there are no payments required up until the home owner moves out of the home, dies or offers it. You have to join therapy with a HUD-approved counselor that focuses on residence equity conversion home loans. " When individuals are doing these reverse home loans they need the money a lot they mark down the negative points that might take place," she said. Search other possibilities, she encourages, such as offering your home so you can utilize the money for a less-expensive residential or commercial property or to rent out.

Exactly How To Safeguard On Your Own: Reverse Mortgages

HECMs generally offer you larger car loan breakthroughs at a reduced total cost than exclusive loans do. In the HECM program, a borrower normally can reside in an assisted living facility or various other clinical facility for up to 12 consecutive months before the car loan have to be paid back. Tax obligations and insurance still should be paid on the car loan, as well as your home needs to be kept. A financial analysis of your readiness as well as capacity to pay property taxes and house owner's insurance. House Equity Conversion Mortgages are federally-insured reverse home mortgages and are backed by the U.

The actuaries that help the lending institution, and you can wager they're not mosting likely to shed money on the offer. As well as since a reverse home mortgage is only letting you use a percentage of the value of your home anyway, what takes place when you reach that limit? But even then, you're not mosting likely to receive the full percentage you get approved for.